Want to boost overseas investment into Australia and increase tax revenue at the same time then – “Why not let non-residents invest in SMSFs provided a certain proportion of their investments are situated in Australia”

There is no doubt that superannuation is taxed at low concessional rates in Australia – 15% for those in accumulation and tax free for those in pension stage. More importantly for those members who are over age 60 and able to access their benefits – any pension or lump sum payments are tax free. Is there any wonder why UK residents are moving to Australia and transferring their pension plans to a qualifying SMSF? Live in Australia – enjoy all that Australia has to offer – pay no tax on income in the fund or when withdrawn post age 60 as opposed to living in the UK and paying tax on pension income at marginal tax rates.

It’s certainly not strange to think of Australia being the world’s best retiree tax haven – provided you have a visa or permanent residency to stay here. In fact, many countries welcome retirees who have financial cash to splash around with special purpose retiree visas. Why not Australia? I think it would be a great idea to let any non-resident invest in Australia through a SMSF and not make the fund non-complying. After all, wouldn’t we be getting investments and tax that we would otherwise miss out on??

But this is not the case, so we are left with a system that makes a non-Australian super fund a non-complying fund. Let’s look at a case study on how the laws work now:

- Case Study- Going Overseas

John Jones is going overseas for a short term holiday but has enquired of a retirement visa in Thailand with the potential loss of the Australian Residency for taxation purposes. What happens to his SMSF and what are the conditions needed to remain a complying SMSF?

- Review of the Law

This question is paramount for income tax purposes.The consequence of being an Australian Superannuation Fund is that the fund includes in its assessable income the ordinary and statutory income the fund derived from all sources, whether in or outside Australia during the income year. If the fund is a complying superannuation fund in relation to the year of income, this income will be taxed concessionally at 15% and entitled to a tax exemption for pension income. However, if the fund is non-complying, the income will be taxed at the highest tax rate, that is 45%.

According to the section 42A of the SIS Act 1993, a complying SMSF is a resident regulated superannuation fund, which is defined as an Australian Super Fund with the meaning of that term in the ITAA 1997.

In that regard section 295-95(2) of the ITAA 1997 provides 3 tests that a fund must satisfy to be treated as an Australian Super Fund:

- the fund is established in Australia or any asset of the fund is situated in Australia;

- the Central Management and Control ( CM&C) of the fund is ordinarily in Australia at a particular time; and

iii. the active member test

Tax Ruling TR 2009/5 provides explanations on these 3 tests. We are going to consider only the CM&C and the active member test as they are the most important when members or trustees go overseas.

The location of the CM&C of the fund is determined by where the high level and strategic decisions of the fund are made and high level duties and activities are performed. It includes the performance of the following duties and activities:

- formulating the investment strategy for the fund;

- reviewing and updating or varying the fund’s investment strategy as well as monitoring and reviewing the performance of the fund’s investments;

- if the fund has reserves – the formulation of a strategy for their prudential management; and

- determining how the assets of the fund are to be used to fund member benefits.

In the majority of cases, the other principal areas of operation of a superannuation fund, such as the acceptance of contributions, the actual investment of the fund’s assets, the fulfilment of administrative duties and the preservation, payment and portability of benefits are not of a strategic or high level nature to constitute CM&C. Rather, these activities form part of the day-to-day or productive side of the fund’s operations.

To be ordinarily in Australia the CM&C must be regularly, usually and customarily exercised in Australia. If the CM&C of the fund is being temporarily exercised outside Australia this will not prevent the CM&C of the fund being ordinarily in Australia at a particular time.

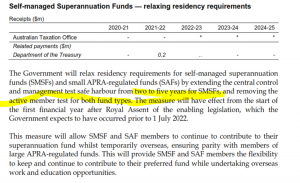

Moreover, subsection 295-95(4) states that the CM&C is ordinarily in Australia at a time even if the CM&C is temporarily outside Australia for a period of not more than 2 years which is to be extended to a generous five years – see Budget Update changes below.

Furthermore, according to the ruling, when there are an equal number of trustees, both in Australia and overseas, who equally participate in the exercise of the CM&C of the fund, the CM&C will ordinarily be in Australia.

In some situations, a person other than the trustee is exercising the CM&C of the fund. Where the trustee of a fund delegates their duties to another person, the delegate will be exercising the CM&C of the fund if they independently and without influence from the trustee, perform those duties and activities that constitute CM&C of the fund. However, if the trustee continues to participate in the high level decision making and activities of the fund by reviewing or considering the decision and actions of the delegate before deciding whether any further or different action is required then it cannot be said that the delegate is exercising the CM&C of the fund. A trustee of a SMSF can bring in a person holding the member’s Enduring Power of Attorney to act as trustee on behalf of the member whilst overseas provided the governing rules of the SMSF allow and the person has been validly appointed.

ATO Ruling Example – person other than trustee exercising CM&C whilst the trustees are overseas

Henry and Eleanor are the trustees of their SMSF, which was established in Australia. The members are Henry and Eleanor. On 29 September 2009, Henry and Eleanor traveled to France to take up management of Eleanor’s family business interests in Europe. They do not have an expected return date, although they do intend to return to Australia at some point in the future. Henry and Eleanor returned to Australia permanently on 22 September 2011.

Prior to moving overseas, Henry and Eleanor arrange for Richard to perform the duties and activities that constitute the CM&C of the fund. During Henry and Eleanor’s absence from Australia, Richard undertakes these activities without reference to Henry and Eleanor. Furthermore, Henry and Eleanor did not participate in any of these high level decision making activities whilst overseas.

In these circumstances, the CM&C of the Superannuation Fund continues to be ordinarily in Australia (by virtue of Richard exercising the CM&C in Australia) within the meaning of paragraph 295-95(2)(b) of the ITAA 1997 at all times during Henry and Eleanor’s absence from Australia.

The other test which needs to be satisfied in order to be treated as an Australian Superannuation Fund is the active member test.

The ‘active member’ test is satisfied if, at the relevant time:

- the fund has no ‘active member’; or

- at least 50% of the total market value of the fund’s assets attributable to superannuation interests held by active members is attributable to superannuation interests held by active members who are Australian residents (subparagraph 295-95(2)(c)(i) of the ITAA 1997); or

- at least 50% of the sum of the amounts that would be payable to or in respect of active members if they voluntarily ceased to be members is attributable to superannuation interests held by active members who are Australian residents (subparagraph 295-95(2)(c)(ii) of the ITAA 1997).

An active member is:

- a contributor to the fund at that time; or

- an individual on whose behalf contributions have been made

A non-active member is:

- a foreign resident: and

- is not a contributor at that time, and

- the only contributions made to the fund on his/her behalf since he/she became a foreign resident were made in respect of a time when he/she was an Australian resident.

ATO Ruling Example: Not an active member

Ally, who is the single member of her SMSF goes overseas on a holiday in July 2009 for an indefinite period of time. She ceases being an Australian resident in July 2011. Before travelling overseas, Ally worked as a fitness instructor at the local health & fitness centre. Her employer failed to make any superannuation contributions in respect of the period of work performed by Ally in the quarter prior to her departure (April to June 2009). In August 2012, Ally’s former employer paid the superannuation guarantee charge to the Tax Office which then distributes the shortfall component of the charge to Ally’s SMSF in September 2012. Ally makes no personal contributions to her SMSF during her absence from Australia.

As Ally is not a resident of Australia from July 2011 and the contribution, that is the shortfall component of the superannuation guarantee charge was made to the SMSF on her behalf in respect of the April-June 2009 period when she was a resident, Ally does not become an active member because of the contribution.

Note: The 2021 Budget proposes for a removal of the active member test. At this time we are unsure if it relates to only the temporary non-residents (soon to be up to five years) or all potential members which leaves open the door for non-residents to own SMSFs as active membership was the roadblock to contributing to super. See the Budget details at the end of this article.

- Transferring from Foreign superannuation funds to Australia

As noted earlier foreign superannuation funds are an important factor for expatriates migrating to Australia. Each year there are literally thousands of former US, European, UK and Asian residents, now living in Australia who can access their superannuation benefits from a foreign superannuation fund. Some may have only just packed up and moved here while others may have been here for decades. The taxation issue is obviously an important one.

IMPORTANT BUDGET UPDATE

Adviser Question to Abbott & Mourly Lawyers

I have a question concerning the tax treatment of lump sums and pensions paid to a 54 year old engineer who has become an Australian resident from a foreign super fund. The client received advice from a major accounting firm stating that the contribution limit caps applied.

We are not so sure and would welcome your thoughts.

Technical Response

There are 4 possible outcomes.

- Lump sum within six months of residency

If the client receives a lump sum from a foreign super fund in respect of foreign employment whilst a non-resident and that lump sum is paid within 6 months of becoming an Australian resident then there is no tax. In that regard a foreign superannuation fund is a superannuation fund that is not an Australian superannuation fund. The laws relating to lump sums from a foreign superannuation fund are found in section 305-60 and 305-65 of the Income Tax Assessment Act 1997. In short, the payment of a lump sum within a six-month period is neither assessable nor exempt income (that is it is tax free) provided it meets the conditions of these sub-sections. It cannot be rolled over as it is not a Roll-over superannuation benefit pursuant to section 306-10 as it comes from a non-complying superannuation fund.

As the amount is not taxable – he has the option of contributing the amount into super, the caps on contributions – $27,500 concessional contributions per annum and $110,000 non-concessional contributions per annum or $330,000 for 3 years, will apply to the amount if he chooses to contribute it into super. He can keep it tax free of course.

- Lump Sums after six months

If he receives a lump sum from a foreign fund more than 6 months after becoming an Australian resident he is taxed on the accrued earnings that arose after becoming a resident unless he chooses to roll over the benefit.

For many migrants to Australia this is the most common practice as many overseas superannuation funds do not necessarily allow the withdrawal of superannuation benefits pre-retirement. A person cannot simply go to the fund when they leave their country and get their superannuation benefits (in Australia you still have to meet a condition of release under the preservation rules). As such members of foreign superannuation funds generally have to wait until a specific time or event such as retirement or aged 55 to claim their offshore superannuation monies. It is only recently that some foreign jurisdictions allow the transfer of superannuation benefits from a local fund to an Australian superannuation fund.

In terms of lump sum payments post six months, section 305-70 of the Income Tax Assessment Act 1997 provides that lump sums received from a foreign superannuation fund will be assessable. The method is complex, however in short it is the applicable fund earnings relative to the time that the member is a resident that will become assessable income and taxed at marginal tax rates with no tax offsets. Applicable fund earnings exclude concessional and non-concessional contributions. As it is not an Australian superannuation fund benefit they cannot access tax free super benefits post age 60.

One of the reasons for taxing the growth accrued in the foreign superannuation fund since residency is that the lump sum has been accumulating in a foreign superannuation fund that is probably tax free in its own jurisdiction – such as the UK and the US, which taxes end benefits not on contributions or fund income.

Of course after paying any tax on the foreign superannuation fund benefits, the member may contribute the net proceeds into a SMSF. The contribution will consist of concessional (if a tax deduction is claimed) or a non-concessional component. One of the problems if it is a large amount may be the contribution caps noted above.

- Rolling-over benefits

If the client receives a foreign superannuation fund lump sum payment after six months, then the member can choose to roll the amount into a complying fund and the super fund is taxed on the earnings that arose after the member became a resident. This will depend on the jurisdiction where the payment is coming from – many do not allow the transfer of pension monies to offshore pension funds. The UK with its Qualifying Overseas Pension scheme allows transfers provided the governing rules of the fund meet certain criteria. These criteria became stricter in 2020 with no ability for the fund to have members receive benefits, under any circumstances until aged 55 plus deeds may need to be reviewed by HMRC – however the LightYear Docs trust deed has just passed such a review.

Section 295-200(2) and 305-80 of the Income Tax Assessment Act 1997 provides that a member can transfer the tax liability that is the assessable income amount determined under 2. above, to the trustee of the superannuation fund. It can be part or the whole of the applicable fund earnings.

Rolling over amounts into super does not appear to be the same as making a direct contribution to the fund. A different set of rules applies. It is clear that section 305-80 of the Income Tax Assessment Act 1997 states that if there is a rollover, then section 295-200 applies. Subsection 295-200(2) provides that where the member has chosen to transfer their tax liability to the trustee of the fund then this amount is assessable income of the fund.

As noted earlier the concessional contribution limit is $27,500. The excess above the concessional contribution limit is taxed as income in the hands of the individual at their marginal tax rate. Concessional contributions are defined in section 292-25 as any contribution to the super fund that is included in the super fund’s assessable income but does NOT include an amount mentioned in 295-200(2) ie the rollover of foreign super see subparagraph 292-25(2)(c)(i).

As far as the non-concessional contributions they are $110,000 per annum. A non-concessional contribution is defined in section 292-90 as a contribution that is made into a super fund and is NOT included in the assessable income of the superannuation fund. Section 295-200 clearly states that the foreign super transferred is included in the assessable income of the super fund but remember only the assessable component.

Note: You can only transfer the amount that is the “applicable fund earnings” (the assessable amount), hence any other amount transferred (that relates to pre-residency) would be a non-concessional contribution and caught by section 292-80.

Hence, the limits do NOT apply to the assessable amount transferred to the super fund. It forms part of the fund’s taxable income and is taxed according to section 295-10 and would be taxed at the low rate (15%). It is only non-arm’s length income and non-TFN contributions that are taxed at higher rates.

When the superannuation benefits are paid from the SMSF, they will consist of taxable or tax free components. A tax-free component is defined under section 307-210 and includes the contributions segment. The contributions segment is found in section 307-220 and is so much of any contributions made into the fund that are not assessable income. In the foreign superannuation fund case this would be amounts where the lump has been contributed to the SMSF and no deduction claimed on the contribution or where the tax liability of the foreign superannuation fund payment has not been transferred under section 305-80 of the Income Tax Assessment Act 1997 – see above. Those amounts where the contribution has been included in assessable income form part of the taxable components. The proportional approach applies in respect of growth for any lump sum draw down or pension payment until age 60 after which lump sums and pensions are tax free – see section 307-125.

- Taking a Pension

If he draws a pension from the foreign fund whilst an Australian resident, it is taxable as income – sub-division 301-B of the Income Tax Assessment Act 1997.