“There is no doubt that creativity is the most important human resource of all. Without creativity, there would be no progress, and we would be forever repeating the same patterns.”

― Edward de Bono, Author, and Lateral Thinker

In the SMSF world never a truer word has been spoken. The industry seems to be filled with lawyers, commentators and advisers who prefer to say “no” or “it’s too hard” or “you have to come to me for advice on how to do that” – even though they then disclaim all liability after weeks and many thousands $$ of fees. No creativity whatsoever, but I guess compliance heads and lawyers tend to look for problems rather than innovate.

A case in point. The government, to its credit and something I have been pushing since the 1990’s, recently increased the number of members in a SMSF to six. This enables the expansion of a SMSF to a family super fund, something that is long overdue. Family super funds are something I have been talking about since the year 2000 and can show the ten benefits to run a Family super fund compared to a simple SMSF. This includes amongst others, the whole family being able to house their superannuation benefits in one fund thereby decreasing costs, family group SMSF insurance, separate investment strategies akin to wrap accounts for members, testamentary trusts flowing from the SMSF rather than the estate, paying sickness benefits and much more. The creative innovation will continue, in my mind anyway but we see such backward looking headlines, generally from the legal profession, such as these:

– 6-MEMBER FUNDS COULD SPELL A ‘RECIPE FOR DISASTER’

– REGULATOR TIPPED TO SCRUTINISE 6-MEMBER FUNDS FOR BEST

– INTERESTS

– 6-MEMBER SMSFS ‘A SOLUTION LOOKING FOR A PROBLEM’

– LIABILITY RISKS HIGHLIGHTED WITH 6-MEMBER SMSFS

But on the other hand, there are some smarter advisers who deal in the real world:

– 6-MEMBER SMSFS TO REDUCE COMPLIANCE COSTS, SAYS IGTO

– SIX-MEMBER FUND LIMIT GETS TRACTION WITH SMSF CLIENTS

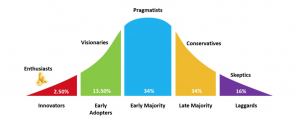

Are you an Early Adopter or a Laggard?

Diagram One on the product or service life cycle is simple. For those that have not seen it, we start with an idea then innovate, create, and develop that idea into a service or product which enables the early adopters to take advantage of it. After a while, the idea or strategy gains momentum before the early majority take it up. Eventually, it flows to the late majority and then eventually the laggards. However, I have to say laggards are laggards and may take centuries to change.

Another case in point. The push to cloud computing saw many early adopter accountants use Xero and other cloud computing and accounting platforms. It then started moving into the early majority but there were still many holding out, worrying about security and other issues, preferring to keep all data on premises. Then came COVID and with that lockdowns and border closes which really shifted the needle and forced even the laggards to move. You cannot hold off change forever.

Diagram One: The Life Cycle of a Strategy, Service, or Idea

BDBNs are a laggard product.

We have all heard of a binding death benefit nomination in terms of superannuation estate planning. They have been around forever and are at the laggard end of the product and service spectrum. There has been a lot written on it, lots and lots of cases challenging them, and the Commissioner of Taxation (who regulates SMSFs) even talks about the use of BDBNs and SMSFs in SMSFD 2008/3, noting:

“Section 59 of the Superannuation Industry (Supervision) Act 1993

(SISA)and regulation 6.17A of the Superannuation Industry

(Supervision) Regulations 1994 (SISR) do not apply to

self-managed superannuation funds (SMSFs).”

Now that is a turn up for the books. The Commissioner is saying the BDBN laws do not apply to SMSFs.

So, who is a BDBN for?

Industry and retail superannuation funds, where members are not involved in the decision-making process. Without a BDBN the Trustee of the superannuation fund would have complete discretion and a long decision-making process as to how a deceased member’s superannuation benefits are to be paid. As a result, there is such a huge backlog of cases in the superannuation division of the Australian Financial Complaints Authority. The former Superannuation Complaints Tribunal had more than 10,000 death benefit cases for review prior to going to AFCA. After all, any dependant or executor of the deceased’s legal estate can challenge an APRA fund trustee’s decision-making process in relation to the payment of death benefits. Unless there is a BDBN!

And then we have experienced SMSF specialist lawyers such as Daniel

Butler from DBA Lawyers who stated:

“We really have this system now that there’s a lot of BDBNs out there

and very rarely does a BDBN pass our scrutiny that it is actually

unchallengeable. We often find reasons to pick apart or pull

apart and undermine BDBNs because they haven’t been done for

one reason or another.”

Now you can’t see me while I am writing this, but I am screaming and

pulling my hair out in exasperation. Why would ANY adviser prepare or

recommend a BDBN for an SMSF when:

- The Commissioner of Taxation has issued a determination that the BDBN laws do not apply to SMSFs

- DBA lawyers and “No Win – No Fee” lawyers presumably will challenge in courts ALL BDBNs produced by any lawyer, adviser, or administrator.

And if an adviser gets it wrong there can be an action under section 54C and 55(3) of SISA to recover losses and damages from any person who has missed out on the faulty BDBN.

A Better Way for the Early Adopters

Normal estate planning deals with how to distribute a testator’s estate upon their death and involves the use of a Will. SMSF estate planning is the creation of a plan on how to distribute a member’s superannuation benefits in a written plan.

The Commissioner of Taxation SMSFD 2008/3 has stated his views:

The payment of death benefits from a superannuation fund is determined in accordance with the governing rules of the superannuation fund and not in accordance with the terms of the deceased’s will. A member can make a death benefit nomination that is a binding direction on the trustee of an SMSF if that is provided for in the governing rules of the fund.

In short, the Commissioner has ruled that a member of a SMSF can make a set of directions, gifts and bequests of their superannuation estate, in much the same way as their Will, provided it is allowed under the Fund’s deed or governing rules.

The SMSF Will

SMSF Will means any document accepted by the Trustee of the Fund dealing with the transfer of a Member’s Superannuation Benefits in the event of a member’s death. A SMSF Will is binding as upon the Trustee, both past, present, and future.

Each trust deed and set of governing rules will have a different description of a SMSF Will and what it means. Many SMSF deeds do not provide for SMSF Wills and are still offering the challengeable BDBN.

At LightYear Docs, where we innovate and create SMSF tools for advisers, our SMSF Will document, which is tied into and forms part of the Fund’s governing rules, states the following about a SMSF Will:

An SMSF Will, consisting of a set of binding directions (see SMSFD 2008/3), is an important legal document that becomes part of the governing rules of the fund detailing how a member seeks to provide superannuation death benefits to their dependents, non-dependants, or legal estate in the event of their death. In creating an SMSF Will, amongst others, there are several possibilities:

- – The provision of a superannuation lump sum — by way of cash or specific assets to dependants and/or the deceased member’s legal estate;

- – The payment of a superannuation income stream to dependants (as defined for taxation purposes) of a deceased member subject to SISA;

- – The payment of a reversionary superannuation income stream to a dependant subject to SISA. A reversionary pension is the continuation of an existing superannuation pension that was payable to a deceased member of the fund;

- – The payment of an adult child dependants benefits directly to the child or to an SMSF Testamentary Trust to protect the benefits and protect from any legal challenge to the estate; and

- – Where a member of an SMSF has more than one superannuation interest in a fund consisting of varying tax-free/taxable components — the choice of allocating from these interests to various dependants and non-dependants.

Six Component Parts to an SMSF Will

In the next part of this series, we will look at the six key components of a SMSF Will and why each is so important and reliant on another. The six components in headline form are:

1. Revocation of prior SMSF Wills and BDBNs – how can you prove which is which if the earlier is not revoked.

2. Reversionary pension to take precedence or not [1]

3. Will the member’s executor or their legal personal representative take the deceased member’s place as trustee of the Fund as per section 17A(3)

4. How are the deceased’s superannuation benefits to be distributed and will they go direct, go to an SMSF testamentary trust, be used to fund a pension, or go to the estate? If the primary beneficiary is not alive or renounces their entitlement who is the next beneficiary and so on.

5. Who is the adviser to the deceased’s SMSF estate? This is a binding forward services contract.

6. If the fund is held to be non-complying what is the default option?

7. For a full detailed analysis including what an SMSF Will looks like watch this training video: https://youtu.be/kmWGsrFi8zA

[1] This is an interesting one and it appears it may be illegal under the Corporations

Act to offer a reversionary pension that then is terminated with a BDBN.